Legislative Updates

As members of the National Association of REALTORS® and California Association of REALTORS®, REALTORS® have benefit of belonging to the largest trade associations dedicated to the promotion and preservation of the real estate profession and the property rights of all. It is this commitment that unifies members in the support or opposition of legislation which may affect the real estate industry as a whole, as well as the communities in which we live, work, and play. We invite you to take a closer look at the important legislation currently being sponsored and/or monitored and share any thoughts and/or comments with your REALTOR® or elected representative to be sure your voice is heard.

C.A.R. Sponsored Bills 2025

(Status as of 2/24/2025)

C.A.R. Makes Its Presence Felt On California Ballot Initiatives

12/04/2024

Successful Outcomes

CAR has had a very successful year campaigning for and against ballot initiatives, including its own direct campaign efforts and efforts funded by its Issue Mobilization Political Action Committee (IMPAC). Together, C.A.R. and IMPAC funded campaigns in the March and November elections. Those efforts led to victory on state ballot measure contests and on more than 40 local measures.

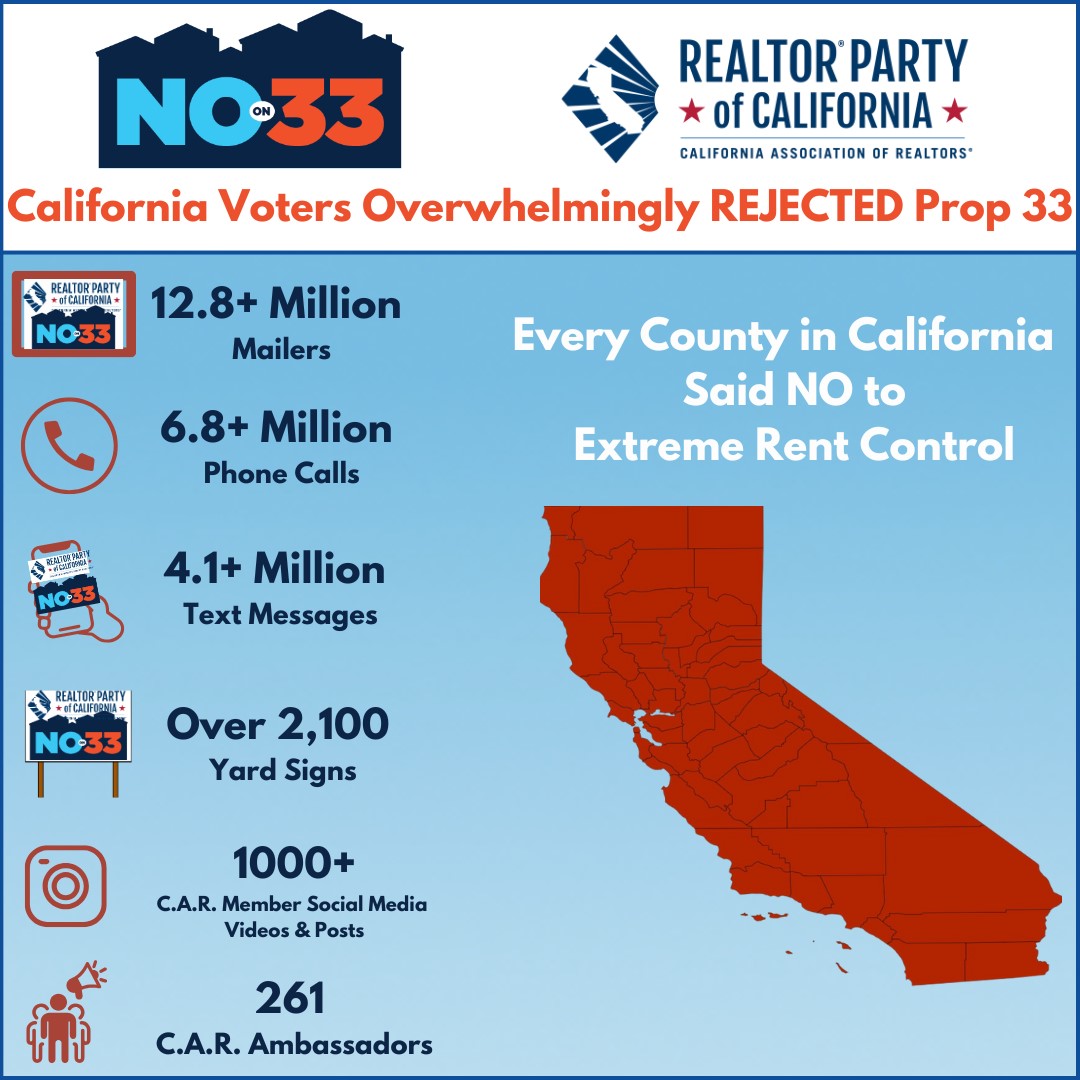

C.A.R.’s campaign against Proposition 33 through its Homeownership for Families, No on 33 Committee, which was partially funded by IMPAC, was essential to the overwhelming defeat of the measure. C.A.R’s campaign included sending over 12.8 million targeted mailers to California voters, texts and phone calls and a robust member mobilization campaign (read more about the results).

IMPAC also contributed the second largest amount of funds to the successful Yes on Prop 34 campaign, sponsored by the California Apartment Association. This initiative, which would require public health care organizations such as the AIDS Healthcare Foundation (the primary funder of the initiatives to repeal Costa-Hawkins), to spend their funds on their core mission.

At the local level, IMPAC funded many campaigns, several of which were in high-profile contests. All funding came at the request of local Associations of REALTORS® who were very involved. More than two dozen local associations contributed to the campaigns to defeat proposed vacant property taxes in Adelanto and South Lake Tahoe, both of which were defeated. Local IMPAC funding helped local associations defeat proposed rent control measures in Marin County, a parcel tax in National City, and a transfer tax proposal in St. Helena.

Not all campaigns were in opposition. Local IMPAC funds also helped local associations pass a flood control assessment in Stockton that will help avoid steep increases in flood insurance, as well as a school bond in Arcadia and in Rancho Palos Verdes.

These are just a few of the many local ballot measure campaigns in which local IMPAC funding was instrumental.

{kind=link}

Recognition of C.A.R’s Effectiveness

C.A.R.’s success also caught the attention of other interested parties in California state politics, especially the media. A recent article published in the online political news site, Politico, placed C.A.R second on a list of “Seven Players Who Left Their Mark on the Ballot Measure Scene this Year.” C.A.R. is described as having “tanked” Prop 33 and “flexing its muscles on local races across the state.” The profile adds that C.A.R. “helped break political fundraising records” and “tilted the scales” against rent control initiatives in Marin County.

Another article in Politico also references how C.A.R.’s political muscle influenced outcomes. The article entitled, “Gavin’s Ballot Scorecard” credits Governor Gavin Newsom with having “killed rent control in California” with his low-key endorsement of the No on Prop 33 campaign. It states that while Newsom did little to promote his opposition, the work done by the No on Prop 33 campaign amplified that opposition. The article describes how “his face was plastered on ads and mailers advocating for a vote against Proposition 33,” and voters were “seeing him in ads arguing the initiative would roll back Newsom’s achievements in affordable housing.” These ads are largely credited with determining the outcome of the vote against the measure.

While the article does not expressly mention C.A.R., it features a photograph of the C.A.R. mailer touting Newsom’s opposition. C.A.R.’s Homeownership for Families, No on 33 Committee sent 3.3 million copies of that flyer to registered Democratic voters in California.

Further recognition of our efforts came in the form of press that might be perceived as adverse to C.A.R, but in politics that can still be a compliment. For example, the San Francisco editorial, Endorsement: Prop 5 limits affordable housing locations. Vote No , objects to how the negotiations on Proposition 5 between the proponents of the initiative and C.A.R changed the resulting initiative. Those changes protected homes and Proposition 13 and took C.A.R. to a neutral position, but as a result of the changes, the SF Chronicle said it had to oppose Proposition 5. In acknowledging C.A.R.’s role in shaping these outcomes, the editorial also states the obvious – that C.A.R. is a powerful and consequential player in the California political arena.